Page 29 - Union Budget_2019

P. 29

Union Budget 2019

CHAPTER VIA DEDUCTIONS

6.1 Deduction under Section 80LA for units of IFSC

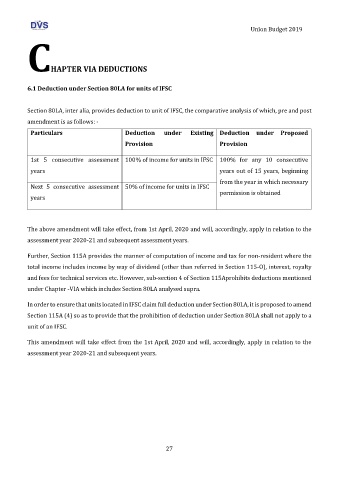

Section 80LA, inter alia, provides deduction to unit of IFSC, the comparative analysis of which, pre and post

amendment is as follows: -

Particulars Deduction under Existing Deduction under Proposed

Provision Provision

1st 5 consecutive assessment 100% of income for units in IFSC 100% for any 10 consecutive

years years out of 15 years, beginning

from the year in which necessary

Next 5 consecutive assessment 50% of income for units in IFSC

permission is obtained

years

The above amendment will take effect, from 1st April, 2020 and will, accordingly, apply in relation to the

assessment year 2020-21 and subsequent assessment years.

Further, Section 115A provides the manner of computation of income and tax for non-resident where the

total income includes income by way of dividend (other than referred in Section 115-O), interest, royalty

and fees for technical services etc. However, sub-section 4 of Section 115Aprohibits deductions mentioned

under Chapter -VIA which includes Section 80LA analysed supra.

In order to ensure that units located in IFSC claim full deduction under Section 80LA, it is proposed to amend

Section 115A (4) so as to provide that the prohibition of deduction under Section 80LA shall not apply to a

unit of an IFSC.

This amendment will take effect from the 1st April, 2020 and will, accordingly, apply in relation to the

assessment year 2020-21 and subsequent years.

27