Page 51 - Union Budget_2019

P. 51

Union Budget 2019

10.14 Relaxation in conditions of special taxation regime for offshore funds

Earlier for offshore funds, there were many instances of fund manager not being in India because of the fact

that the fund manager shall constitute permanent establishment (PE) of offshore funds in India.

The Government, in order to provide relief for such offshore funds, inserted Section 9A whereby the fund

manager being in India and carrying out fund management activities on behalf of offshore funds, would per

se not constitute PE subject to certain specified conditions. These conditions are relating to residence of

fund, corpus, size, investor broad basing, investment diversification and payment to fund manager at arms'

length.

Various representations were made to relax few conditions in order to ensure effective working of offshore

funds through fund managers.

Thus, it is proposed to amend Section 9A to change the conditions relating to corpus of the fund and

remuneration of eligible fund manager.

The conditions pre and post amendment are as follows: -

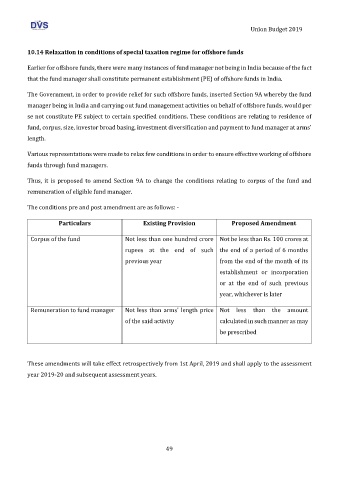

Particulars Existing Provision Proposed Amendment

Corpus of the fund Not less than one hundred crore Not be less than Rs. 100 crores at

rupees at the end of such the end of a period of 6 months

previous year from the end of the month of its

establishment or incorporation

or at the end of such previous

year, whichever is later

Remuneration to fund manager Not less than arms' length price Not less than the amount

of the said activity calculated in such manner as may

be prescribed

These amendments will take effect retrospectively from 1st April, 2019 and shall apply to the assessment

year 2019-20 and subsequent assessment years.

49