Page 9 - Budget_2020

P. 9

Union Budget 2020

Profits and Gain from Business or Profession

Deduction u/s 35AD is Optional

Sec 35AD, provides for 100% deduction for capital expenditures by specified business. Currently, it seems

mandatory to avail incentive under this section for specified businesses.

Amend Sec 35AD to make it optional.

Further, it is proposed that deduction of capital expenditure shall be denied under any other section only if the

deduction is claimed by the assessee and it is allowed under this section

AY 2020-21 and subsequent AYs

This amendment has been proposed to clarify a possible interpretation issue whereby it seemed mandatory to

opt for deduction u/s 35AD, failing which the assessees would be denied deduction in the normal course.

Allowing Deduction for Amount Disallowed u/s 43B, to Insurance Companies on Payment Basis

Sec 43B allows certain expenses only if they are paid within the due date for filing tax returns. For payments

beyond the due date - deduction shall be allowed in the year of payment.

There was ambiguity in applying the above provision to insurance companies, which is now being clarified.

AY 2020-21 and subsequent AYs

Extension of Concessional Tax Regime for Generation of Electricity

Various stakeholders requested to provide the benefit of the concessional rate of 15% u/s 115BAB to business

of generation of electricity.

Scope of the benefit shall include companies engaged in generation of electricity

AY 2020-21 and subsequent AYs

The above proposal would foster the generation of electricity which is imperative for all the sectors of the

economy. In the last 5 years, the electricity generation has increased from 1048.67 billion units in 2014 to

1249.34 billion units in 2019. However, it shall be noted that the benefit is extended only to power generation

companies and not distribution entities.

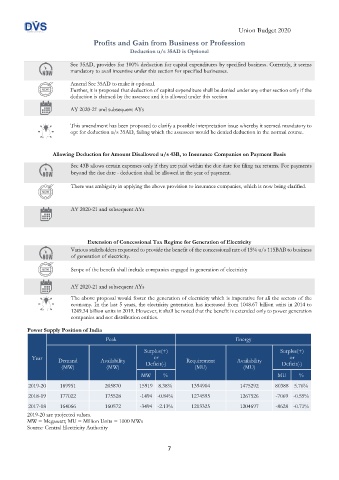

Power Supply Position of India

Peak Energy

Surplus(+) Surplus(+)

Year Demand Availability or Requirement Availability or

(MW) (MW) Deficit(-) (MU) (MU) Deficit(-)

MW % MU %

2019-20 189951 205870 15919 8.38% 1394904 1475292 80388 5.76%

2018-19 177022 175528 -1494 -0.84% 1274595 1267526 -7069 -0.55%

2017-18 164066 160572 -3494 -2.13% 1213325 1204697 -8628 -0.71%

2019-20 are projected values.

MW = Megawatt; MU = Million Units = 1000 MWs

Source: Central Electricity Authority

7