Page 28 - Budget_2020

P. 28

Union Budget 2020

Solution

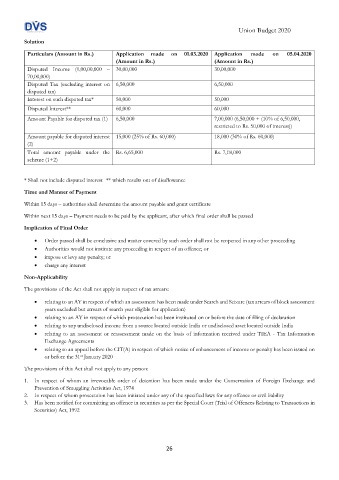

Particulars (Amount in Rs.) Application made on 01.03.2020 Application made on 05.04.2020

(Amount in Rs.) (Amount in Rs.)

Disputed Income (1,00,00,000 – 30,00,000 30,00,000

70,00,000)

Disputed Tax (excluding interest on 6,50,000 6,50,000

disputed tax)

Interest on such disputed tax* 50,000 50,000

Disputed Interest** 60,000 60,000

Amount Payable for disputed tax (1) 6,50,000 7,00,000 (6,50,000 + (10% of 6,50,000,

restricted to Rs. 50,000 of interest))

Amount payable for disputed interest 15,000 (25% of Rs. 60,000) 18,000 (30% of Rs. 60,000)

(2)

Total amount payable under the Rs. 6,65,000 Rs. 7,18,000

scheme (1+2)

* Shall not include disputed interest ** which results out of disallowance

Time and Manner of Payment

Within 15 days – authorities shall determine the amount payable and grant certificate

Within next 15 days – Payment needs to be paid by the applicant, after which final order shall be passed

Implication of Final Order

• Order passed shall be conclusive and matter covered by such order shall not be reopened in any other proceeding

• Authorities would not institute any proceeding in respect of an offence; or

• impose or levy any penalty; or

• charge any interest

Non-Applicability

The provisions of the Act shall not apply in respect of tax arrears:

• relating to an AY in respect of which an assessment has been made under Search and Seizure (tax arrears of block assessment

years excluded but arrears of search year eligible for application)

• relating to an AY in respect of which prosecution has been instituted on or before the date of filing of declaration

• relating to any undisclosed income from a source located outside India or undisclosed asset located outside India

• relating to an assessment or reassessment made on the basis of information received under TIEA - Tax Information

Exchange Agreements

• relating to an appeal before the CIT(A) in respect of which notice of enhancement of income or penalty has been issued on

or before the 31 January 2020

st

The provisions of this Act shall not apply to any person:

1. In respect of whom an irrevocable order of detention has been made under the Conservation of Foreign Exchange and

Prevention of Smuggling Activities Act, 1974

2. In respect of whom prosecution has been initiated under any of the specified laws for any offence or civil liability

3. Has been notified for committing an offence in securities as per the Special Court (Trial of Offences Relating to Transactions in

Securities) Act, 1992

26