Page 20 - Union Budget, 2022

P. 20

Union Budget, 2022

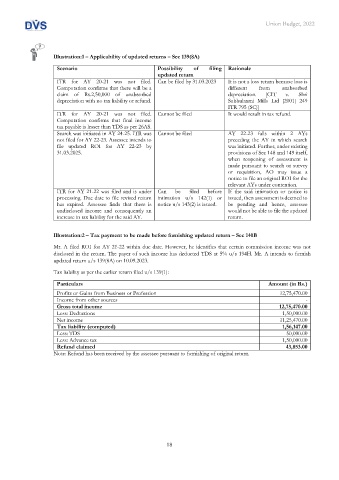

Illustration:1 – Applicability of updated returns – Sec 139(8A)

Scenario Possibility of filing Rationale

updated return

ITR for AY 20-21 was not filed. Can be filed by 31.03.2023 It is not a loss return because loss is

Computation confirms that there will be a different from unabsorbed

claim of Rs.2,50,000 of unabsorbed depreciation. [CIT v. Shri

depreciation with no tax liability or refund. Subhulaxmi Mills Ltd [2001] 249

ITR 795 (SC)]

ITR for AY 20-21 was not filed. Cannot be filed It would result in tax refund.

Computation confirms that final income

tax payable is lesser than TDS as per 26AS.

Search was initiated in AY 24-25. ITR was Cannot be filed AY 22-23 falls within 2 AYs

not filed for AY 22-23. Assessee intends to preceding the AY in which search

file updated ROI for AY 22-23 by was initiated. Further, under existing

31.03.2025. provisions of Sec 148 and 149 itself,

when reopening of assessment is

made pursuant to search or survey

or requisition, AO may issue a

notice to file an original ROI for the

relevant AYs under contention.

ITR for AY 21-22 was filed and is under Can be filed before If the said intimation or notice is

processing. Due date to file revised return intimation u/s 142(1) or issued, then assessment is deemed to

has expired. Assessee finds that there is notice u/s 143(2) is issued. be pending and hence, assessee

undisclosed income and consequently an would not be able to file the updated

increase in tax liability for the said AY. return.

Illustration:2 – Tax payment to be made before furnishing updated return – Sec 140B

Mr. A filed ROI for AY 21-22 within due date. However, he identifies that certain commission income was not

disclosed in the return. The payer of such income has deducted TDS at 5% u/s 194H. Mr. A intends to furnish

updated return u/s 139(8A) on 10.09.2023.

Tax liability as per the earlier return filed u/s 139(1):

Particulars Amount (in Rs.)

Profits or Gains from Business or Profession 12,75,470.00

Income from other sources -

Gross total income 12,75,470.00

Less: Deductions 1,50,000.00

Net income 11,25,470.00

Tax liability (computed) 1,56,147.00

Less: TDS 50,000.00

Less: Advance tax 1,50,000.00

Refund claimed 43,853.00

Note: Refund has been received by the assessee pursuant to furnishing of original return.

18