Page 31 - Union Budget, 2022

P. 31

Union Budget, 2022

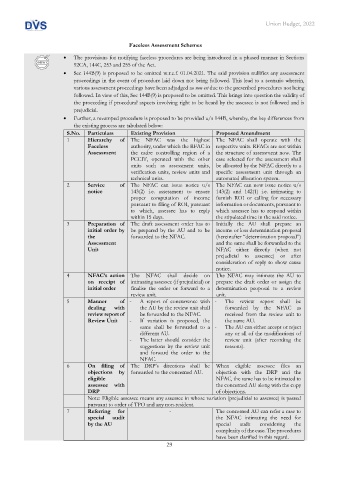

Faceless Assessment Schemes

• The provisions for notifying faceless procedures are being introduced in a phased manner in Sections

92CA, 144C, 253 and 255 of the Act.

• Sec 144B(9) is proposed to be omitted w.r.e.f. 01.04.2021. The said provision nullifies any assessment

proceedings in the event of procedure laid down not being followed. This lead to a scenario wherein,

various assessment proceedings have been adjudged as non est due to the prescribed procedures not being

followed. In view of this, Sec 144B(9) is proposed to be omitted. This brings into question the validity of

the proceeding if procedural aspects involving right to be heard by the assessee is not followed and is

prejudicial.

• Further, a revamped procedure is proposed to be provided u/s 144B, whereby, the key differences from

the existing process are tabulated below:

S.No. Particulars Existing Provision Proposed Amendment

1 Hierarchy of The NFAC was the highest The NFAC shall operate with the

Faceless authority, under which the RFAC in respective units. RFACs are not within

Assessment the cadre controlling region of a the structure of assessment now. The

PCCIT, operated with the other case selected for the assessment shall

units such as assessment units, be allocated by the NFAC directly to a

verification units, review units and specific assessment unit through an

technical units. automated allocation system.

2 Service of The NFAC can issue notice u/s The NFAC can now issue notice u/s

notice 143(2) i.e. assessment to ensure 143(2) and 142(1) i.e. intimating to

proper computation of income furnish ROI or calling for necessary

pursuant to filing of ROI, pursuant information or documents, pursuant to

to which, assessee has to reply which assessee has to respond within

within 15 days. the stipulated time in the said notice.

3 Preparation of The draft assessment order has to Initially the AU shall prepare an

initial order by be prepared by the AU and to be income or loss determination proposal

the forwarded to the NFAC. (hereinafter “determination proposal”)

Assessment and the same shall be forwarded to the

Unit NFAC either directly (when not

prejudicial to assessee) or after

consideration of reply to show cause

notice.

4 NFAC’s action The NFAC shall decide on The NFAC may intimate the AU to

on receipt of intimating assessee (if prejudicial) or prepare the draft order or assign the

initial order finalise the order or forward to a determination proposal to a review

review unit. unit.

5 Manner of - A report of concurrence with - The review report shall be

dealing with the AU by the review unit shall forwarded by the NFAC as

review report of be forwarded to the NFAC. received from the review unit to

Review Unit - If variation is proposed, the the same AU.

same shall be forwarded to a - The AU can either accept or reject

different AU. any or all of the modifications of

- The latter should consider the review unit (after recording the

suggestions by the review unit reasons).

and forward the order to the

NFAC.

6 On filing of The DRP’s directions shall be When eligible assessee files an

objections by forwarded to the concerned AU. objection with the DRP and the

eligible NFAC, the same has to be intimated to

assessee with the concerned AU along with the copy

DRP of objections.

Note: Eligible assessee means any assessee in whose variation (prejudicial to assessee) is passed

pursuant to order of TPO and any non-resident.

7 Referring for - The concerned AU can refer a case to

special audit the NFAC intimating the need for

by the AU special audit considering the

complexity of the case. The procedures

have been clarified in this regard.

29